Weekend Update #270

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

Global markets remained under pressure this week as escalating tensions in the Middle East triggered declines across both equities and bonds. U.S. stocks notched a fourth consecutive weekly loss—their longest slide in a year—as investors reassess expectations for a short-lived conflict and instead confront a prolonged disruption to global energy markets. Oil prices surged, with Brent briefly topping $112, driven by the near-closure of the Strait of Hormuz and mounting concerns over supply chain disruptions. Natural gas prices also jumped following strikes on key Gulf infrastructure, reinforcing fears of sustained energy-driven inflation.

Rates markets repriced sharply in response. Sovereign yields moved higher globally, with U.S. Treasuries selling off as markets fully priced out Federal Reserve rate cuts in 2026 and began hedging for potential hikes. This shift reflects growing concern that persistent energy shocks will feed through to broader inflation, tightening financial conditions even as geopolitical risks weigh on growth. Meanwhile, second-order risks—including potential disruptions to semiconductor supply chains tied to energy instability in Taiwan—added another layer of concern for global markets.

The Iran conflict entered its third week with no signs of de-escalation, continuing to drive both humanitarian and economic fallout. Iran intensified attacks across the Persian Gulf, targeting critical energy infrastructure in Saudi Arabia, the UAE, and Qatar, including a strike on the Ras Laffan LNG complex, bringing shipping through the Strait of Hormuz to a near standstill.

The U.S. is weighing more aggressive intervention, including a potential plan to seize or blockade Kharg Island, Iran’s primary oil export hub, while deploying additional Marines to the region. Donald Trump indicated openness to dialogue with Iran but signaled opposition to a ceasefire, underscoring the risk of further escalation. Efforts to build a multinational coalition to secure the Strait have seen limited traction, with key allies hesitant to deepen involvement. Iran, meanwhile, has reaffirmed its intent to target regional energy assets, reinforcing expectations that the conflict could stretch from weeks into months.

Recent data highlighted an already firm inflation backdrop. U.S. producer prices rose 0.7% in February, driven by services, suggesting underlying price pressures were building even before the surge in energy costs. Central banks responded cautiously but with a more hawkish tilt. The Federal Reserve held rates steady at 3.5%–3.75% while maintaining its outlook for one cut in 2026, citing heightened uncertainty. In contrast, the Bank of England held at 3.75% but signaled readiness to hike if inflation proves persistent, prompting markets to price in additional tightening and contributing to the global rise in yields.

On the corporate front, Meta Platforms Inc. announced a $27 billion agreement with Nebius Group NV to secure long-term AI infrastructure capacity, underscoring continued acceleration in AI-related capex. In digital assets, Bitcoin’s rally was supported by sustained ETF inflows, signaling renewed institutional engagement. Elsewhere, rising concern around semiconductor supply chains—particularly in Taiwan—highlighted the growing risk of geopolitical disruptions feeding into critical technology and manufacturing ecosystems.

Friday’s Close (Weekly Performance)

S&P 500 6,506.48 (-1.90%)

Nasdaq 21,647.61 (-2.07%)

Dow Jones 45,577.41 (-2.11%)

Thank you Blue Room Senior Analyst NICK PEART.

Federal Reserve Chairman Jerome Powell

Good afternoon. My colleagues and I remain squarely focused on achieving our dual mandate goals of maximum employment and stable prices for the benefit of the American people. The U.S. economy has been expanding at a solid pace. While job gains have remained low, the unemployment rate has been little changed in recent months, and inflation remains somewhat elevated.

Today, the FOMC decided to leave our policy rate unchanged. We see the current stance of monetary policy as appropriate to promote progress toward our maximum employment and 2 percent inflation goals. The implications of developments in the Middle East for the U.S. economy are uncertain. We will remain attentive to risks to both sides of our dual mandate. I will have more to say about monetary policy after briefly reviewing economic developments.

Available indicators suggest that economic activity has been expanding at a solid pace. Consumer spending has been resilient, and business fixed investment has continued to expand. In contrast, activity in the housing sector has remained weak.

In our Summary of Economic Projections, the median participant projects that real GDP will rise 2.4 percent this year and 2.3 percent next year, somewhat stronger than projected in December.

In the labor market, the unemployment rate was 4.4 percent in February and has changed little since late last summer. Job gains have remained low. A good part of the slowing in the pace of job growth over the past year reflects a decline in the growth of the labor force, due to lower immigration and labor force participation, though labor demand has clearly softened as well. Other indicators, including job openings, layoffs, hiring, and nominal wage growth, generally show little change in recent months.

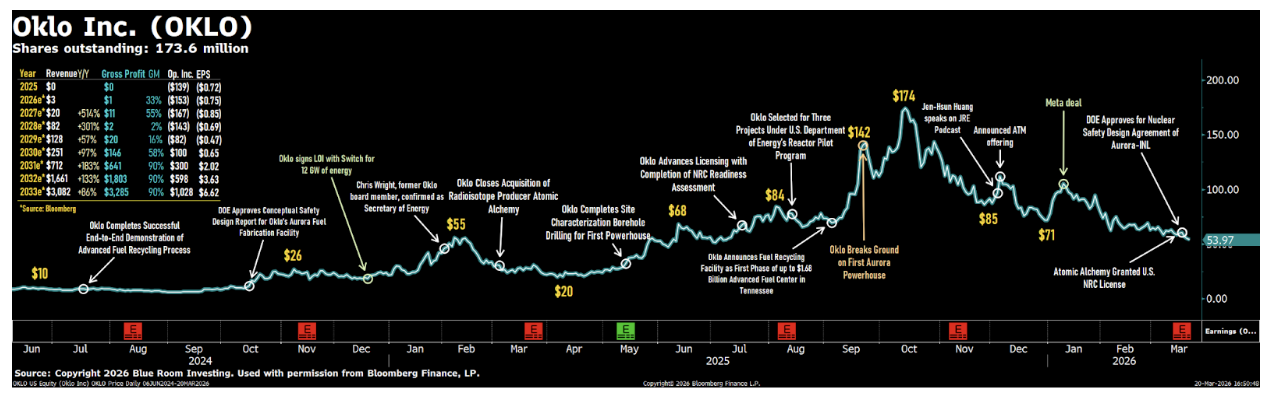

Jacob DeWitte — Co-Founder, Chief Executive Officer & Chairman

2025 was a step change year for Oklo. We transitioned from product development into active project deployment across all of our business units.

During the year, we broke ground on our first Aurora Powerhouse at Idaho National Laboratory under the DOE's Reactor Pilot Program, advanced key commercial partnerships across the value chain, including our early 2026 prepayment agreement with META to support plans for a 1.2-gigawatt power campus, and began initial construction activities on A3F at INL. We also completed the acquisition of Atomic Alchemy and made substantial construction progress at Groves in Texas, our first radioisotope test reactor.

In fuel, we completed fast-spectrum plutonium criticality experiments, supporting using plutonium as a bridge fuel. We announced the first phase of our advanced fuel center in Tennessee, and we progressed licensing activities across multiple assets. Taken together, 2025 was the year Oklo turned our platform strategy into deployed projects while also strengthening the balance sheet to fund that execution and our long-term growth.

Before I go deeper into execution, it is also important to understand how much the external environment shifted over the last two years. In 2024 and 2025, US nuclear policy moved toward a more execution-oriented posture across licensing, asset deployment, fuel supply, and capital formation. You can see the four main pillars here.

First, executive actions and regulatory direction focused on accelerating licensing and enabling first-of-a-kind projects.

Second, federal support mechanisms, including tax credits, loan guarantees, and direct financing tools are improving the pathway to fund projects.

Third, fuel sovereignty measures are pushing domestic capability across the conversion, enrichment, HALEU, and strategic fuel materials.

And fourth, implementation of the ADVANCE Act is aimed at reducing friction and licensing and enabling more efficient deployment pathways.

The policy backdrop has shifted from a light tailwind to a very strong tailwind for the nuclear sector, and Oklo is positioned to move in that environment.

Going forward, we will talk about Oklo through three integrated business units, power, fuel, and isotopes, that together form a unique vertically integrated nuclear platform. Power is the clean baseload power and heat from our sodium fast reactors that can utilize a broad spectrum of fuels. Fuel provides Oklo with an integrated pathway to produce fuel required for our powerhouses as well as for our peers and competitors. This de-risks deployment, strengthens long-term supply, and unlocks nuclear energy abundance at scale through fuel recycling. And isotopes expand the platform into high-value products and services with strategic domestic importance that are natural co-products from our other business units. The key point is that integration across the value chain is designed to unlock multiple complementary value streams over time.

Naresh Tanna

Chief of Staff to CEO & Head of Investor Relations

Thank you. Welcome to Precision BioSciences PBGENE-DMD Investor Update.

I'm Naresh Tanna, Head of Investor Relations, and I'm joined by my fellow members of Precision's Management team, including Alex Kelly, Chief Financial Officer, and Dr. Cassie Gorsuch, Chief Scientific Officer. We are also joined by our co-presenters and esteemed members of the Key Opinion Leader community, including Pat Furlong, founder of Parent Project Muscular Dystrophy, also known as PPMD, a leading DMD Advocacy Organization. We're also joined by Dr. Aravindhan Veerapandiyan, leading DMD investigator and pediatric neurologist at Arkansas Children's Hospital. Next slide, please.

Before we begin, I'd like to thank you for your support. Before we begin, I'd like to remind everyone that our remarks today may contain forward-looking statements. These statements are based on current expectations, and actual results could differ materially. Please refer to our latest 10-K and 10-Q filings for a detailed discussion of those risk factors. Next slide, please.

Without further ado, I'd like to hand it off to Alex Kelly.

Alex Kelly

Chief Financial Officer

Thank you very much, Naresh, and thank you again for everybody for joining our call this morning. We can go to the next slide and just cover a little bit of an intro to Precision BioSciences for those who may not be familiar with the company.

Our company was founded in 2006 as a spin-out from Duke University. Our co-founders, including Jeff Smith, who's our chief research officer, developed a novel platform called ARCUS, which is designed with the goal of treating and curing difficult-to-treat diseases with high unmet need, including rare genetic diseases such as Duchenne muscular dystrophy. Our platform is proprietary. We own more than 75 patents that cover the ARCUS and in vivo gene editing. And as I mentioned earlier, it's wholly owned by Precision BioSciences.

There are a number of different gene editing tools that are available. Many people know CRISPR. ARCUS is not CRISPR. CRISPR is derived from bacterial sources, whereas ARCUS is derived from a homing endonuclease, I-CreI, which is found in green algae. So it has a lot of features that help differentiate ARCUS from other gene editing tools, including its size, the way that it cuts, and its simplicity. Those are the three differentiating characteristics of ARCUS. But ultimately, it's all about helping patients and improving function. Next slide, please.

One of the things that we've seen and demonstrated over the last 15 to 20 months is that ARCUS as a platform works. ARCUS works in a variety of settings. We've seen this demonstrated from our partners in vivo gene editing, such as iECURE. And iECURE is using an ARCUS nuclease developed by Precision BioSciences for a gene insertion program for neonatal OTC deficiency, a rare disease that unfortunately has very dire consequences for the infants who are born with this disease. iECURE has been in the clinic for more than a year. And in that time, they've demonstrated that they have a complete clinical response in the very first patient who is treated with ECUR-506. iECURE also expects to give further updates on their programs in the first half of 2026.

Next, we saw proof that ARCUS works in ex vivo gene editing. We saw this demonstrated in the cancer setting by Imugene, who's partnering with us and taking azer-cel forward for oncology. We've also seen very good progress made by TG Therapeutics using azer-cel for autoimmune diseases such as multiple sclerosis. Both of those trials are ongoing right now and we look forward to seeing more results from both of those.

We've also demonstrated on our own that PBGENE-HBV for chronic hepatitis B works for its desired goal as well. PBGENE-HBV is being studied in the ELIMINATE-B trial, which is studying in chronic hepatitis B. You may know that chronic hepatitis B is a very large disease. It affects some 300 million people around the world. Also, over the course of 20 to 30 years, it often results in serious liver complications such as cirrhosis and or liver cancer. So with our PBGENE-HBV program, we've been in the clinic for a little over a year now. We've treated 13 patients so far across five cohorts and we've administered more than 30 doses of PBGENE-HBV. We have additional clinical data expected this year. I think that I would direct investors to look at the major medical conferences that are focused on hepatitis B. And the first opportunity for major conferences, probably the EASL conference coming up at the end of May. So we'll be giving more and further updates on the ELIMINATE-B program at that conference.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.