Weekend Update #269

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

Equity markets ended the week lower as U.S. and Israeli attacks on Iran continued to dominate sentiment. The energy supply shock rippled through risk appetite, with wild swings in oil prices throughout the week — Brent crude spiked to $119 per barrel on Monday as the Strait of Hormuz closure affected roughly 20% of global oil supply, before settling at $103 per barrel on Friday. Over the past month, the price of Brent crude has now risen 56%. In response to the supply shock, the International Energy Agency announced a record 400 million coordinated barrel release from the strategic reserves of its 32 members, more than double the 183 million barrels released following Russia’s invasion of Ukraine. Equities were quick to respond to commentary coming from the Trump administration, but markets struggled to weigh the positive signals that the conflict could come to an end soon against escalation in strikes throughout the week. The S&P 500 closed Friday at its lowest level since November 2025, while the CBOE volatility index at 27.19 remained elevated.

As of Friday, the U.S. reported that the new supreme leader of Iran, Mojtaba Khamenei, has been wounded in recent strikes, but that didn’t stop his first public statement vowing that the Strait of Hormuz would remain closed as Iran seeks vengance for strikes. Reports have indicated that 7 ships have been attacked in the Strait of Hormuz and the Persian Gulf so far, with suggestions that Iran will begin laying mines in the Strait to further shut traffic. At least 20 liquefied natural gas carriers are currently trapped in the Persian Gulf, accounting for around half of LNG ships available for charter. The Trump Administration messaged on Friday that military escorts of ships through the Strait will occur at some point but only after its main military objectives have been accomplished.

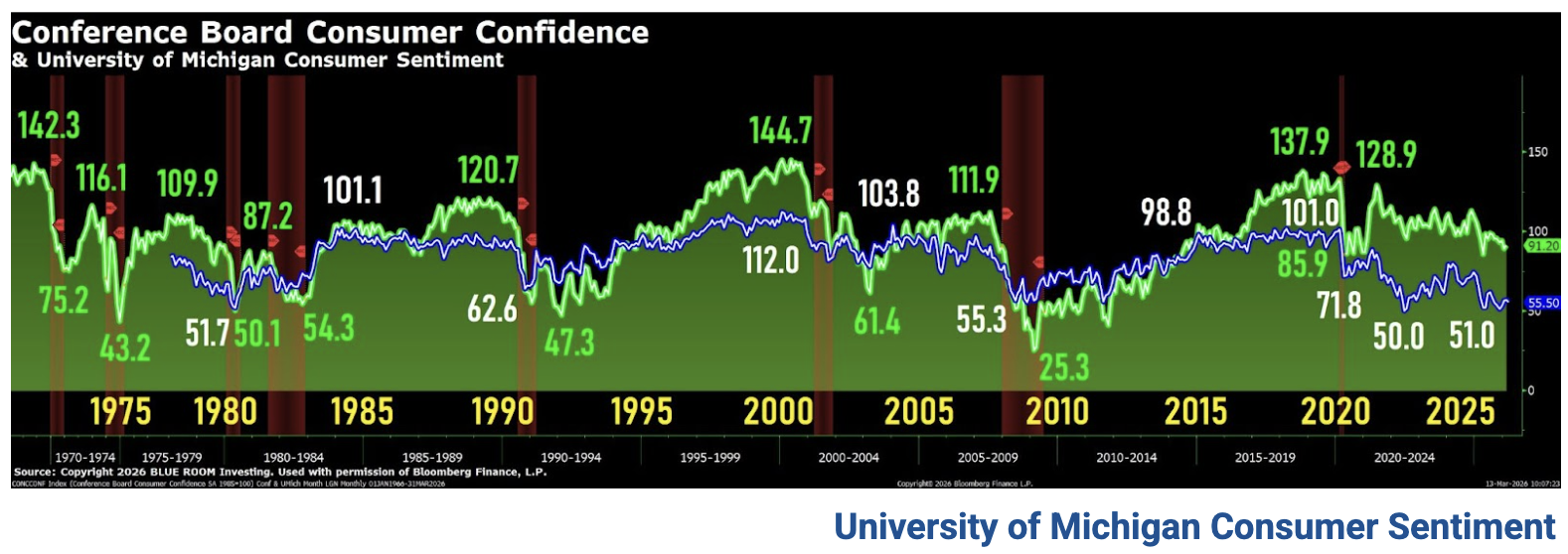

In economic data for the week, the February CPI report showed headline inflation rose 0.3% MoM and 2.4% YoY, while core inflation rose 0.2% MoM and 2.5% YoY. Initial Jobless Claims at 213,000 for the week ended March 7, below the 215,000 consensus estimate and still below the highs of 2025. The PCE price index for January showed 0.1% MoM and 2.8% YoY headline inflation, while core inflation rose 0.4% MoM and 3.1% YoY. The second release of Q4 2025 GDP showed the economy grew at 0.7% QoQ, below the prior 1.4% reported in the first release, due to contracting federal government spending. Real Personal Spending in January rose 0.1% MoM, slightly above the 0.0% expectation but that still revealed pressure on consumer demand. The University of Michigan Consumer Sentiment report for March was slightly higher than economist estimates but still fell to the lowest level of 2026 as the Iran War weighed on 12-month expectations for gas prices and personal finances. The JOLTS Job Openings report showed a positive surprise on available jobs at 6.95 million, suggesting continued stabilization in the labor market to start the year.

Overall, key economic indicators largely showed stabilization in the labor market and inflation but will be at risk if the war in Iran is extended. The balance of risks places the Federal Reserve in a tougher position to cut interest rates this year. Last Friday, the market was pricing a full rate cut by September 2026 and two by July 2027. These expectations have shifted to pricing the first rate cut by March 2027 and only reaching two cuts by December 2027.

Key earnings reports this week included Oracle, which beat consensus estimates and raised its guidance as demand for AI infrastructure continues to surge. The results were a show of confidence at a time when investors had become more cautious about its investment levels that hinge on a continuation of the AI boom. Adobe also reported earnings that exceeded consensus estimates, including AI-first ARR that more than tripled YoY. Still, shares came under pressure in trading on Friday as 18-year CEO Shantanu Narayen announced plans to step down as CEO, introducing some uncertainty for investors about the company’s path forward amid AI-disruption in the industry.

Friday’s Close (Weekly Performance)

S&P 500 6,632.19 (-1.60%)

Nasdaq 22,105.36 (-1.26%)

Dow Jones 46,558.47 (-1.99%)

Thank you Blue Room Senior Analyst JARED FENLEY

Consumer sentiment dipped about 2% to 55.5, reaching its lowest reading of the year.

Interviews completed prior to the military action in Iran showed an improvement in sentiment from last month, but lower readings seen during the nine days thereafter completely erased those initial gains.

Gasoline prices have exerted the most immediate impact felt by consumers, though the magnitude of pass-through to other prices remains highly uncertain.

A broad swath of consumers across incomes, age, and political affiliation all reported declines in expectations for their personal finances, down 7.5% nationally.

Interviews for this release were collected between February 17 and March 9, with about half completed after the start of the U.S. military conflict in Iran.

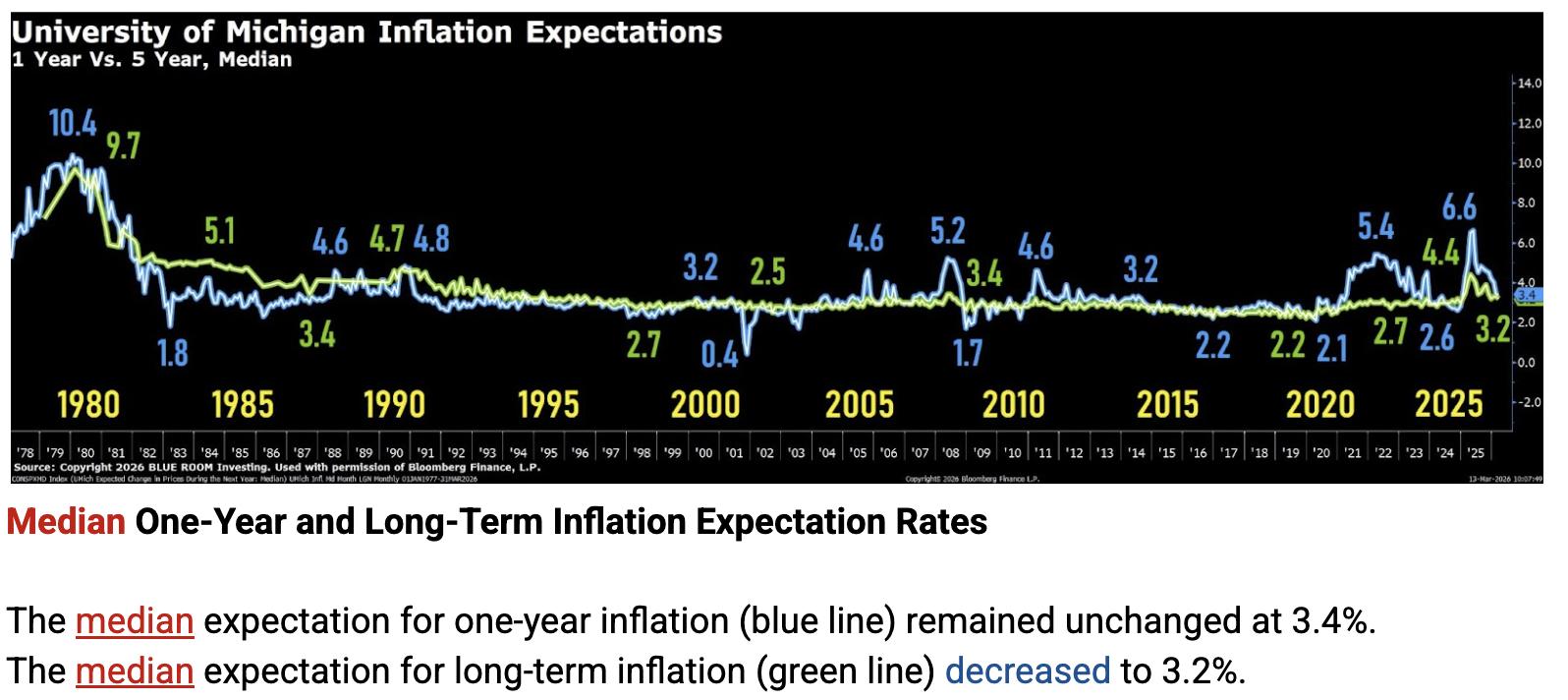

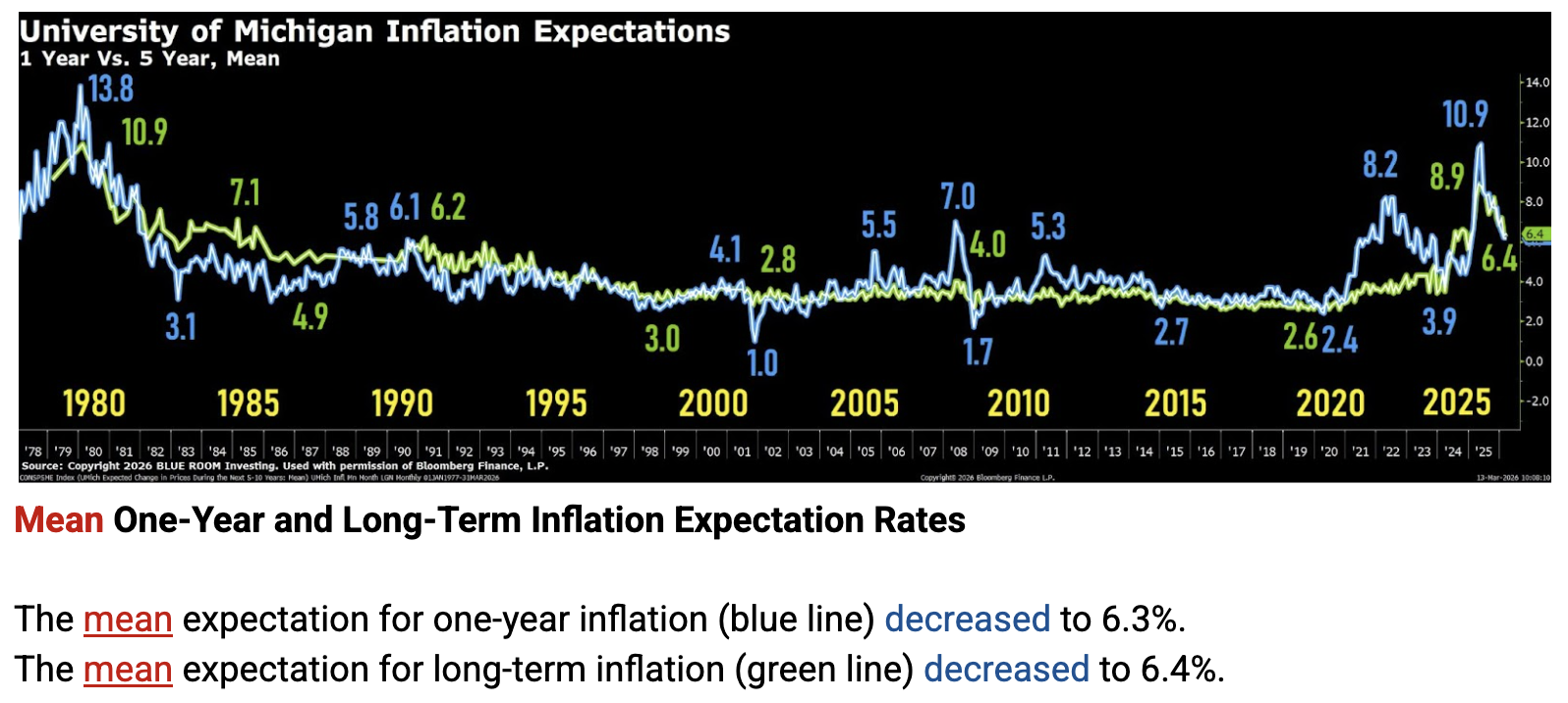

This month, year-ahead inflation expectations ended six months of consecutive declines, stalling at 3.4%. The current reading exceeds those seen in 2024 and remains well above the 2.3-3.0% range seen in the two years pre-pandemic. Long-run inflation expectations inched down to 3.2%. In 2024, readings ranged between 2.8% and 3.2%, while in 2019 and 2020, they were consistently below 2.8%. Note that for both time horizons, interviews completed after February 28th exhibited higher inflation expectations than those completed before that date.

Highlights:

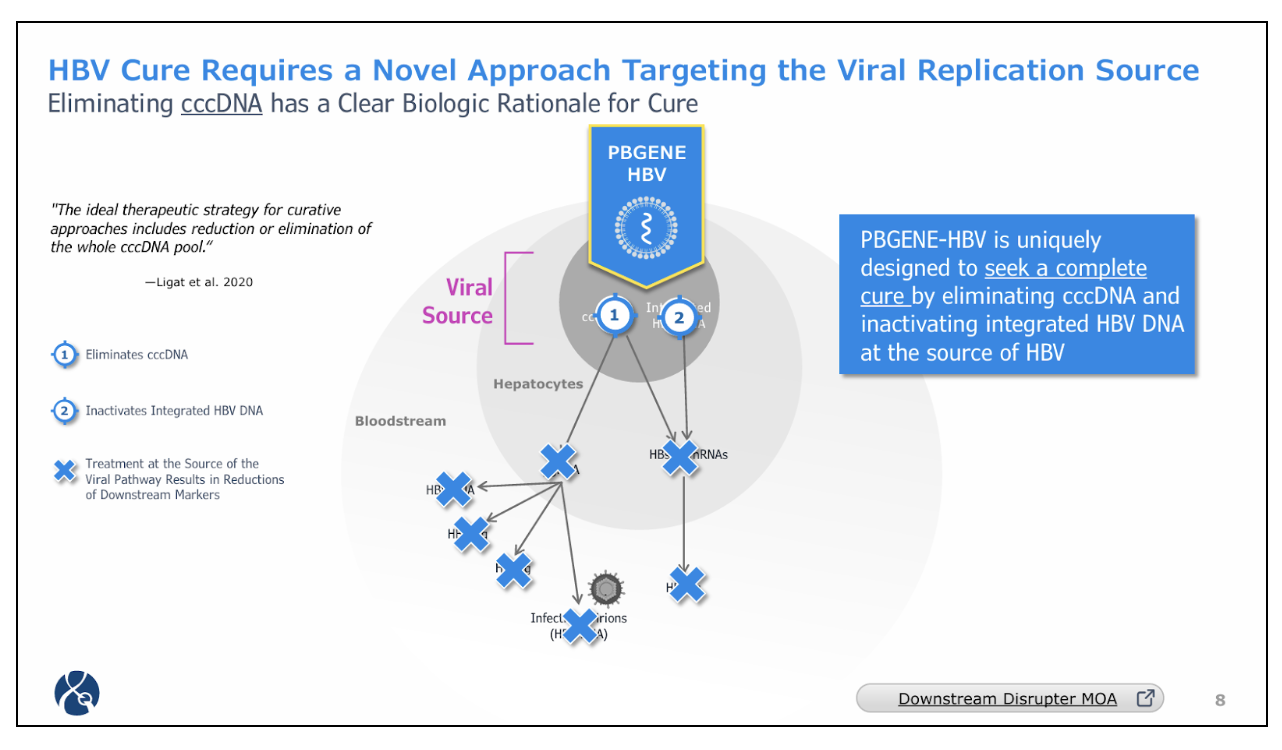

PBGENE-HBV Phase 1 data featured Late Breaker presentation at AASLD, The Liver Meeting, showing safety, tolerability, and cumulative, dose-dependent antiviral activity

Strong Phase 1 ELIMINATE-B trial execution for PBGENE-HBV with 13 patients now dosed across the first 5 cohorts

Data updates expected at medical conferences throughout 2026

Received IND Clearance for PBGENE-DMD, enabling IRB and site activation for Phase 1/2 FUNCTION-DMD trial

Data from multiple patients expected by year-end 2026

Raised $75 Million in November 2025, extending expected cash runway through multiple clinical inflection points between 2026 and the end of 2028

“2025 was an exceptional year for Precision BioSciences marked by meaningful clinical and financial progress. We delivered on what we committed to achieve and more in 2025 positioning Precision BioSciences for success in 2026 and beyond,” said Michael Amoroso, Chief Executive Officer. “The evidence supporting the clinical utility of ARCUS for in vivo gene editing continues to mount in diseases with high unmet need led by advancement of PBGENE-HBV through multiple cohorts in our ELIMINATE-B study for chronic hepatitis B.

At The Liver Meeting 2025, we presented late-breaking clinical data showing safety and cumulative, dose-dependent antiviral activity along with paired biopsy findings that provide the first molecular evidence consistent with viral DNA gene editing in patients. In another first, our partner iECURE achieved a complete response in the first infant with neonatal onset OTC deficiency following treatment with ECUR-506 which utilizes an ARCUS nuclease developed by Precision for in vivo gene insertion.”

“Additionally, our team completed all Investigational New Drug (IND) enabling activities for PBGENE-DMD and filed an IND application by the end of 2025 after announcing prioritization of the program in May 2025. This paved the way for the IND clearance in early 2026 and allowed us to begin the IRB process to activate clinical trial sites,” continued Mr. Amoroso. “Finally, we strengthened our financial position by extending our expected cash runway through 2028 and entered 2026 focused on achieving multiple potential clinical value-inflection points for PBGENE–HBV and PBGENE–DMD this year.”

Wholly Owned Portfolio

PBGENE-HBV (Viral Elimination Program):

Wholly owned in vivo gene editing program under investigation in a global Phase 1 first–in–human clinical trial, designed to be a potentially curative treatment for chronic Hepatitis B infection. In patients with chronic hepatitis B, cccDNA acts as the template to make new infectious viral particles. PBGENE–HBV is the only clinical stage program that targets the elimination of cccDNA, the sole source of viral replication, leading to sustained loss of HBV DNA and other downstream viral transcripts.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.