Weekend Update #271

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

The escalating war in Iran and fears about lasting disruption to the global supply chain added to the equity selloff this week, with the S&P 500 marking a 5th consecutive week of losses. Equities started the week on a positive note, with a hopeful message sent by President Trump that the U.S. and Iran had “very good and productive conversations regarding a complete and total resolution of our hostilities”. Throughout the week, Iranian officials rejected the statement, saying there are no negotiations occurring, and the back and forth tension between conflicting reports introduced a new layer of uncertainty. Additional U.S. military deployments were reported, with plans to boost total troops to around 17,000 as of Friday. Late Thursday, President Trump reported an extension in his deadline for negotiations prior to a strike to key Iranian infrastructure to Monday, April 6, at 8 PM Eastern Time, delaying the timeline from the original Friday, March 27 deadline. The market is bracing for the possibility of significant escalation with the U.S. and Israeli forces attempting a “final blow” to Iranian forces, including a potential ground invasion, which sent Brent Crude to $114.17 per barrel on Friday afternoon.

The U.S. 10-Year Treasury yield ended Friday at 4.4278%, the highest since July 16, 2025. The 30-year mortgage rate rose to 6.38%, up sharply after breaking below 6% for the first time since 2022 on February 26. Weekly mortgage applications in the U.S. fell more than 10% for the second consecutive week. Interest rate expectations for year-end 2026 ended Friday at 3.702%, implying a greater chance for rate hikes in the coming year compared to the more than 2 cuts priced in the day before U.S. and Israeli strikes on Iran. With risks building, the S&P 500 ended this week with a P/E multiple of 24.9x, a low since May 2025 but up from the Liberation Day low of 21.3x.

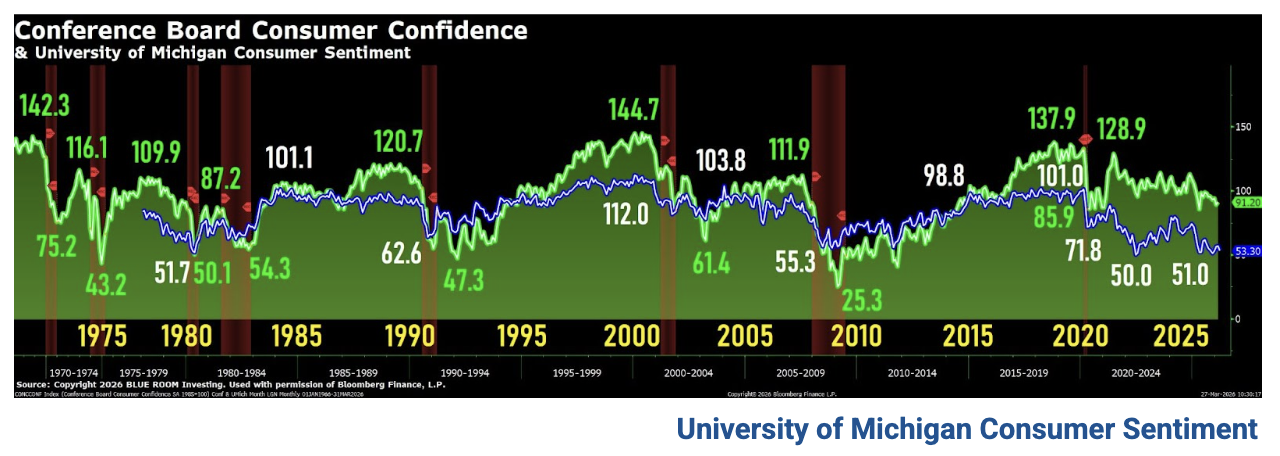

In economic data for the week, the S&P Global flash March composite index fell to 51.4, the weakest growth since April 2025, while input prices for services and manufacturing rose at their fastest paces since May and August, respectively. S&P Global characterized this as an unwelcome combination of slower growth and higher inflation resulting in uncertainty from the conflict with Iran. Initial jobless claims for the week ended March 21 were in line with expectations at 210,000, showing gradual improvements in the labor market since September. The University of Michigan consumer sentiment report showed consumers’ sharpest one-month increase in year-ahead inflation expectations since Liberation Day, while expectations for gas prices in the coming year increased fivefold from February. The pessimism was broad-based among demographic groups and across survey metrics, but the silver lining for the final March report is that consumers expect inflationary impacts to be limited in duration, with long-term expectations well-anchored.

Adding downward pressure to software stocks this week, Amazon Web Services announced it’s developing new AI tools to automate work in sales, business development, cybersecurity, and server networking, aiming to replace the work of thousands of its employees. Google announced its development of TurboQuant this week, which compresses the RAM needs of large language models to reduce memory usage by up to 6 times. Google’s innovation could help to reduce an under-supplied global memory market and caused a selloff in memory makers this week.

Next week, markets will look for any signals of real progress in negotiations with Iran for an off-ramp to the conflict. With the extended April 6 deadline in place, additional troop deployments or details on various scenarios for deploying boots on the ground could add further pessimism over a quick resolution.

Friday’s Close (Weekly Performance)

S&P 500 6,368.85 (-2.12%)

Nasdaq 20,948.36 (-3.23%)

Dow Jones 45,166.64 (-0.90%)

Thank you Blue Room Senior Analyst JARED FENLEY.

Consumer sentiment fell back 6% this month to 53.3 — its lowest level since December 2025.

Declines were seen across age and political party. Consumers with middle and higher incomes and stock wealth, buffeted both by escalating gas prices and volatile financial markets in the wake of the Iran conflict, exhibited particularly large drops in sentiment.

Overall, the short-run economic outlook plunged 14%, and year-ahead expected personal finances sank 10%, while declines in long-run expectations were more subdued. These patterns suggest that, at this time, consumers may not expect recent negative developments to persist far into the future. These views are subject to change, however, if the Iran conflict becomes protracted or if higher energy prices pass through to overall inflation.

Interviews for this release were collected between February 17 and March 23, with about two-thirds completed after the start of the U.S. military conflict in Iran.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.