Weekend Update #264

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

After heavy market selling throughout the week, stocks staged a sharp rebound on Friday, posting their strongest session since May as investors moved to buy the dip amid easing fears around surging AI investment. The S&P 500 jumped 2%, the Dow Jones Industrial Average reached 50,000, and risk assets broadly stabilized, with software stocks rising 3.5% and chipmakers surging 5.7% after Nvidia CEO Jensen Huang said AI demand remains “incredibly high.” Commodities and crypto also bounced, with gold and silver recovering and Bitcoin rebounding above $70,000 after a 50% drawdown from its peak. The volatility followed a selloff reminiscent of the DeepSeek reaction in early 2025, when new automation tools from Anthropic reignited concerns about AI-driven disruption, and comes as markets in 2026 continue to rotate away from megacap growth toward value and more economically sensitive stocks. On the political front, near-term fiscal risk eased after the House approved a Trump-negotiated funding deal to end the partial government shutdown, though another funding deadline looms amid continued negotiations over immigration enforcement.

Economic data remained mixed, with US consumer sentiment unexpectedly rising to a six-month high, driven by wealthier households benefiting from equity gains and reinforcing signs of a persistent K-shaped economy. Year-ahead inflation expectations fell to 3.5%, the lowest in a year, but labor market anxiety increased sharply, with the perceived probability of job loss at its highest level since July 2020, a concern echoed by companies announcing over 108,000 job cuts in January—the most since 2009—alongside record-weak hiring intentions. Meanwhile, January’s ISM Services data pointed to continued expansion but softer momentum, as business activity stayed firm while new orders, employment, and export demand weakened, even as prices paid rose to a three-month high, signaling renewed inflation pressures amid supply-chain shifts and trade policy uncertainty.

Company-specific developments continued to shape sector dynamics. The AI investment cycle remains historically large, with Alphabet, Amazon, Meta, and Microsoft collectively forecasting nearly $650 billion in capital expenditures in 2026 for data centers and related infrastructure—levels expected to rival or exceed their combined spending from the prior three years. At the same time, concerns are mounting that advances in AI-enabled automation could pressure parts of the software industry. The White House is signaling a tougher regulatory stance, with officials weighing a potential antitrust probe into US homebuilders amid housing affordability concerns, while the Justice Department has opened an early-stage review of Netflix’s proposed acquisition of Warner Discovery’s studios and HBO Max, underscoring heightened scrutiny of industry consolidation.

Overall, markets are stabilizing after a violent rotation away from tech, supported by resilient services activity and improving headline sentiment. However, rising job cuts, slowing demand, elevated price pressures, regulatory uncertainty, and extreme volatility in crypto markets point to a fragile equilibrium rather than a decisive return to a risk-on environment.

Friday’s Close (Weekly Performance)

S&P 500 6,932.30. (-0.10%)

Nasdaq. 23,031.21. (-1.84%)

Dow Jones. 50,115.67 (+2.50%)

Thank you Blue Room Senior Analytics NICK PEART.

Jim Anderson — Chief Executive Officer

Thank you, Paul, and thank you, everyone, for attending today's call. As the world's leading innovator and provider of photonic technology and solutions, Coherent is at the center of an extraordinary expansion of optical networking infrastructure that's enabling tremendous growth in data traffic in the scale across, scale-out and scale-up networks of AI data centers. As a result of the AI build-out, we saw strong revenue and profit growth in our December quarter. We also experienced another step-function increase in our bookings, which we expect to increase again in our current quarter.

Given the extraordinary strength and visibility of demand from our customers, combined with our continued rapid expansion and production capacity, we expect a period of sustained strong revenue growth over the coming quarters. In particular, we expect continued strong sequential revenue growth in both our March and June quarters, and we expect our fiscal '27 revenue growth rate to exceed our fiscal '26 growth rate.

The key growth drivers that we see over the coming quarters are growth in both 800 gig and 1.6T transceivers, growth from the ramps of new products such as OCS and CPO solutions and ongoing exceptionally strong demand in our products for DCI and scale across. In addition, we are now seeing demand signals that indicate a pickup in the growth of our industrial business over the course of this calendar year, led by strong orders from our semicap equipment customers. Overall, we're excited about the growth outlook over the coming quarters. We are also focused on driving meaningful operating leverage and expect to continue to deliver EPS growth at a significantly faster than our expected revenue growth rate.

With that overview, let me provide some additional details on our recent quarter and what we expect moving forward. Turning to our Q2 operating results. Revenue increased by 9% sequentially and 22% year-over-year on a pro forma basis, which excludes revenue from our recently divested Aerospace and Defense business. Non-GAAP gross margin expanded by 24 basis points sequentially and 77 basis points year-over-year. The combination of revenue growth and gross margin expansion drove non-GAAP EPS growth of 11% sequentially and 35% year-over-year.

Blue Room

Investment Team Bullpen

Friday

February 6, 2026

9:30 AM

Jared Fenley covers University of Michigan Consumer Sentiment Preliminary February Data.

Do we have green shoots in the soft data?

______________________________________

Copyright 2026 Blue Room (TM) Investing.

Note: There is no AI generated content in this video.

Ryan Taylor — CRO & Chief Legal Officer

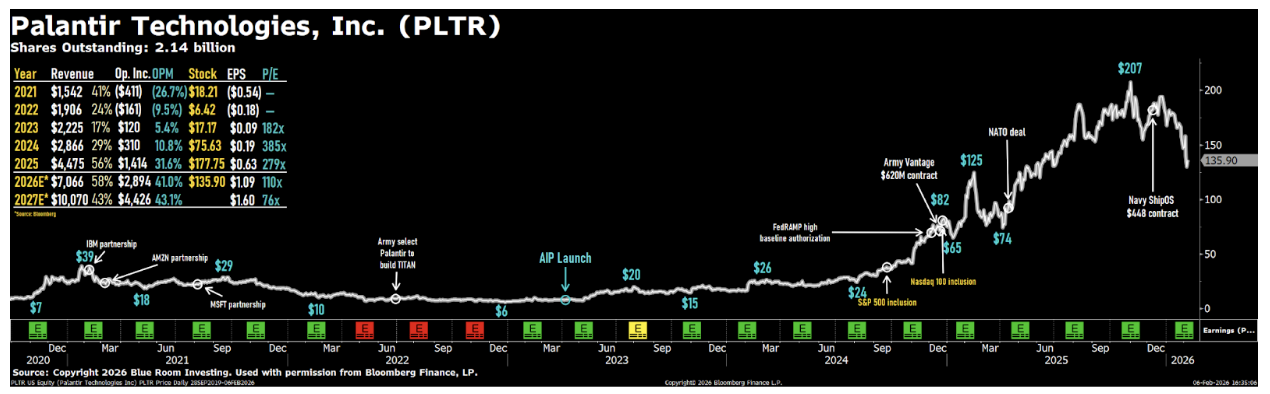

Our fourth quarter results are nothing short of historic, capping off a monumental year for our business. In Q4, overall revenue surged 70% year-over-year, our highest growth rate as a public company, propelled by the relentless momentum of our U.S. business, which now commands 77% of our total revenue, up 93% year-over-year and 22% sequentially. Our Rule of 40 score reached new heights at 127%, up 46 points year-over-year and 13 points quarter-over-quarter, proving that hyper-growth and exceptional profitability aren't mutually exclusive, but rather the inevitable outcome of Palantir delivering transformational impact at scale.

We closed our highest TCV quarter ever at $4.3 billion, and fourth quarter trailing 12-month revenue from our top 20 customers increased 45% year-over-year to $94 million per customer, a testament to our customers' conviction. Our customers aren't tentatively trying AI; they're committing to it at scale with Palantir as the driving force. The rapid advancement of AI models is continuing to drive the commoditization of cognition. The next step is for the market to differentiate between those who are supplying the commoditization of cognition and those who are scaling the leverage made possible by it. We are the only enterprise software company that made a conscious choice to focus exclusively on the latter, delivering real-world value for our customers by maximally leveraging these models in production. Palantir is an n of 1. This is what makes the Rule of 127 possible. This is why customers who have crossed the chasm with Palantir, the AI-haves, are defining the future of their industries, while those still on the other side, the AI-have-nots, are fighting for survival in the present.

As Johnson Controls noted about our work together, "It is really incredible to see that you can transform a 140-year-old company with the power of AI." I'm seeing this play out across our customer base. We are moving customers from AI adopters to AI-native enterprises, transforming execution into exponential advantage. This is summed up best by an executive at Thomas Cavanagh Construction who noted, "We've gone all-in so much so that every other software must justify its existence. And so far, they haven't been able to. 97% of our employees use Foundry every day. Foundry is our operating system." And he continued, "The ontology is the secret weapon. Nothing else comes close. And not only are we getting rid of third-party software, we've replaced their functionality and then beaten them to new features all within the year because of the ontology."

Our U.S. commercial business grew 137% year-over-year and 28% sequentially, building on the blistering pace of 121% year-over-year in Q3 and 93% year-over-year growth in Q2, defying conventional enterprise software dynamics. This isn't just growth, it's compounding acceleration. AIP continues to fundamentally transform how quickly our customers realize value, collapsing the time from initial engagement to transformational impact.

Lear noted at our recent DevCon conference their experience starting with 100 users and 4 use cases and growing to 16,000 users and 280 use cases. We're seeing the effects across our entire customer base. Existing customers are expanding faster and larger. For example, a utility company expanded from $7 million ACV in Q1 2025 to $31 million ACV by year-end, while an energy company expanded from $4 million ACV in Q1 2025 to over $20 million ACV by year-end, driven by value generated from new use cases. In addition, new customers are starting with substantial initial deals. A healthcare company completed two boot camps with us last summer and signed a $96 million deal with us before the end of the year. An engineering services company saw a series of demos in the fall, then signed an $80 million deal before year-end. Speed to production and transformational scale is no longer optional, it's existential. Palantir remains the only platform delivering that speed at enterprise scale.

Steve Huffman — Co-Founder and Chief Executive Officer

Thanks, Jesse. Hi everyone, and thanks for joining our Q4 earnings call. 2025 was a breakout year for Reddit. We surpassed bold targets, built real momentum across our business, improved our unique community model at scale. We crossed $2.2 billion in revenue, up 69% year-over-year and delivered $530 million in net income. In Q4 alone, we welcomed over 121 million daily active users to our platform, up 19% year-over-year and over 471 million weekly active users up 24%.

None of this would be possible without our team. Thank you to our employees for a phenomenal year. The momentum we're seeing across the business, especially in all three sections of our ad funnel, is the result of years of foundational work coming to life. I know, we are all eager to build on the success. The numbers tell just a small part of an important story. Reddit is at the center of a once in a generation shift and it's not a coincidence.

We're now operating in a fundamentally different Internet, one shaped by opaque algorithms, generative content, and growing distrust. And yet, amid this shift, more people are turning to Reddit, not just to aimlessly scroll, but to connect, learn, and research. That's because Reddit is the most human place on the Internet. In a world flooded with AI slop, people are seeking real community, lived experience, and trusted opinions. That's Reddit's differentiator.

To put it simply, more people than ever are coming to Reddit, because Reddit is for everyone. One of the main reasons Reddit is the go-to place for community is the candour of our conversations. This authenticity is rare and it's what makes conversations on Reddit uniquely helpful and influential. But in the age of AI, you can't easily distinguish a real person's thoughts or recommendations from a bot, that trust erodes. That's why we're actively working on ways to preserve our authenticity and conversation quality. This begins the launch of verified profiles for brands and individuals in Q4, and we'll quickly move to bot verification and labeling next. We're making good progress here and are excited to share more updates in the coming weeks.

Our consumer product work remains a top priority, particularly driving user growth, retention and deeper engagement through more seamless experiences. Two areas of especially high priority, improving new user onboarding and integrating our search interfaces. Let's dig into how these are going.

On the onboarding side, we deployed numerous experiments in Q4. We're actively iterating on these learnings and working fast to improve retention for new and casual users. That retention supports growth, engagement, monetization, and more effective marketing.

Next, search. In Q4, we made significant progress in unifying our core search with Reddit Answers, our AI-powered search feature. Together, they drove more search volume and queries per user, with over 80 million people searching directly on Reddit every week in Q4, up from 60 million just a year ago. We released Reddit Answers in five new languages with more on the way, and are piloting dynamic, agentic search results that include media beyond text. Reddit is already where people go to find things, making our platform an end-to-end search destination is how we meet that demand.

As the industry evolves, how we think about our product and users must evolve too. We've historically reported logged-in versus logged-out users, but as some of our work to streamline onboarding, instant personalization, for example, blurs the line between these states, the distinction between them makes less sense. As such, we plan to phase out reporting on logged-in and logged-out later this year.

2026 02 06 Blue Room Investment Team Bullpen – RDDT Q4 2025 Earnings Review

Blue Room

Investment Team Bullpen

Friday

February 6, 2026

9:30 AM

Nick Peart reviews Reddit Q4 2025 earnings results, which came in well ahead of expectations.

______________________________________

Copyright 2026 Blue Room (TM) Investing.

Note: There is no AI generated content in this video.

Subscribe to our weekly newsletter!

Evan Spiegel — Chief Executive Officer

Hi, everyone, and welcome to our call. Last fall, we embarked on a new chapter for our company with the articulation of the crucible moment faced by our business. At that time, we laid out our plans to accelerate and diversify our revenue growth, pivot our business toward more profitable growth and deliver on the commercial launch of Specs in 2026. The impacts of this strategic direction began to manifest in the operating results of our business in Q4 and we are excited to build-on this momentum in the year ahead.

Over the last three years, we have grown monthly active users by more than 150 million, reaching 946 million in the most recent quarter and bringing us within striking distance of our goal to reach 1 billion global monthly active users. We have already achieved immense reach and depth of engagement in many of the world's most attractive advertising geographies, and we believe this affords us a significant opportunity to grow our top-line and expand average revenue per user over-time. Growing our community in these prosperous geographies remains a priority and we remain committed to our long-term goal of reaching 1 billion monthly active users. But going-forward, we will seek to strike a better balance between the pace of community growth and the rate of top-line growth in order to pivot our business to more profitable growth.

For the advertising business, our focus will be on three core initiatives. The first is fostering direct connections between brands and Snapchatters by leveraging our core product capabilities across Snapchat. The second will be making it easier and more performant for advertisers to connect with Snapchatters by leveraging AI tooling and capabilities end-to-end through our ad platform, including creative development, campaign setup, and performance optimization. Finally, we plan to grow our advertiser base by scaling and optimizing our go-to-market operations that support the success of small and medium-sized businesses. Ultimately, we will grade the performance of our advertising business based on the rate of growth in advertising revenue, with a focus on gaining share over-time.

The other revenue portion of our business has become an outsized source of growth and is playing a critical role in diversifying our top-line. In the year ahead, we will focus on growing existing subscription offers, including Snapchat Plus and memory storage plans, while innovating to bring compelling new offers to our platform. This momentum is already materializing with subscribers growing 71% year-over-year to reach 24 million in Q4. In the year ahead, growth in subscribers will be a critical input metric to track our progress and we will ultimately grade our performance-based on the growth at the annualized run-rate for other revenue.

We are focusing on three significant catalysts for gross margin expansion to drive profitable growth. First, with community growth-focused on monetizable markets and with our cost-to-serve increasingly calibrated to the monetization potential of each market, we expect that our infrastructure costs will pivot from being a source of gross margin pressure to become a margin-accretive investment. Second, as more of our ad revenue is derived from higher-margin placements such as sponsored snaps and promoted places, we expect advertising margins to improve. Third, we expect that the growing scale of our subscription business, which is built on a foundation of existing engagement and infrastructure investment will become increasingly accretive to overall gross margins.

2026 02 05 Blue Room Investment Team Bullpen – SNAP Q4 2025 Earnings Review

Blue Room

Investment Team Bullpen

Thursday

February 5, 2026

9:30 AM

Jared Fenley reviews Reddit Q4 2025 earnings results, which came in well ahead of expectations.

______________________________________

Copyright 2026 Blue Room (TM) Investing.

Note: There is no AI generated content in this video.

Subscribe to our weekly newsletter!

Anthony Noto — Chief Executive Officer

Thank you, and good morning, everyone. 2025 was a tremendous year on all fronts. Our member focus drove an unprecedented level of innovation across our business and led to the strongest financial performance in the history of our company. As we begin 2026, we're positioned for another year of unprecedented results and I could not be more excited. We come into the year with a differentiated one-stop shop model with a full suite of products that allow members to borrow, save, spend, invest, and protect better.

A demonstrated track record of driving durable growth through continuous innovation, resulting in compounded annual growth of nearly 50% from $240 million in 2018 to $3.6 billion in 2025. A scaled member base of 13.7 million members, more than 20 times larger than the 650,000 members we had in 2018 and our highest brand awareness ever at nearly 10% versus roughly 2% in 2018. Despite that unprecedented growth, we still have massive addressable markets across our existing businesses and huge opportunities for growth in newer areas like crypto, AI and business banking.

And finally, we have a fortress balance sheet, which we further strengthened through $3.2 billion in new capital, increasing our tangible book value by $2 per share to $7 per share, giving us a broad range of optionality. This gives me great confidence that we will continue to drive durable compounded growth for years to come, resulting in superior financial returns. I will discuss some of what we've planned for the year ahead in a moment. But first, let me begin with our key results for the fourth quarter.

Starting with the drivers of our durable growth. We added a record 1 million new members in Q4, increasing total members by 35% year-over-year to 13.7 million SoFi members. This was our first time adding over 1 million members in a single quarter. We also added a record 1.6 million new products in Q4, increasing total products by 37% year-over-year.

We now have over 20 million products. Cross-buy continues at an exceptional pace with 40% of new products opened by existing SoFi members. Over the past year, our cross-buy rate has increased by 7 percentage points. This clearly demonstrates the effectiveness of our one-stop shop strategy and our ability to build deeper multi-product relationships with members. And as before, we fully leverage new technologies like artificial intelligence. Our strong member and product growth powered our revenue growth in the fourth quarter. Adjusted net revenue was a record at over $1 billion, up 37% year-over-year, marking our first $1 billion quarter.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.