Weekend Update #281

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

Equity markets gained this week, fueled by hopes for a U.S.-Iran peace deal to be signed within the next week. The first half of the week was dominated by fears over escalation in attacks between Israel and Iran. On Tuesday, President Trump stated that a U.S. Apache helicopter was shot down by Iran over the Strait of Hormuz, leading to further U.S. strikes as a response. Following Wednesday’s reports that the U.S. was considering large-scale strikes in order to pressure Iran for a deal, the president announced Thursday that strikes were called off, as the U.S. and Iran had approved final discussions and points for a memorandum of understanding to end the conflict. The fast-changing geopolitical narrative led to big swings in equities, energy markets, and volatility this week, with investors still looking for a finalization of the agreement as soon as Sunday, potentially to be signed in Geneva, Switzerland.

In economic data for the week, all eyes were on the CPI and PPI inflation reports. Wednesday’s May CPI report mainly fell in line with expectations, with headline CPI increasing 0.5% MoM in May and 4.2% YoY, the hottest annual pace since April 2023. Core CPI came in line with expectations at 2.9% YoY while coming in cooler-than-expected on the monthly basis at 0.2%. Energy was the biggest contributor to the index’s rise, stemming from continued conflict and disruption in the Strait of Hormuz. Services, goods, and food prices showed broad stability, which investors took as a positive signal that energy spikes are not spilling over to other categories in a price spiral. Thursday’s PPI report was hotter-than-expected on headline price changes, rising 1.1% MoM in May and 6.5% YoY. Excluding food and energy, PPI rose 0.4% MoM and 4.9% YoY, both cooler-than-expected.

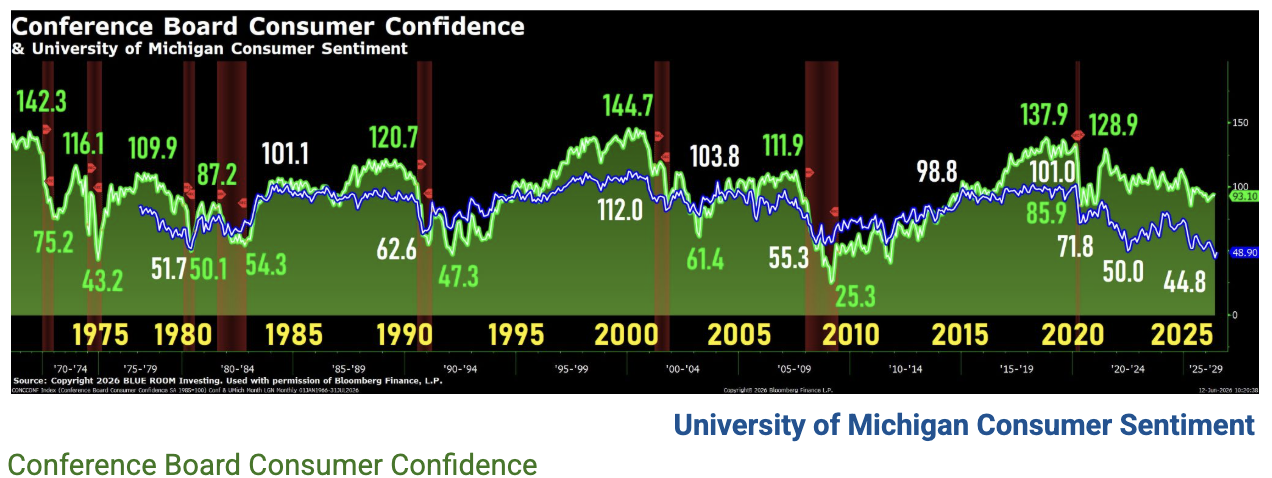

The May NFIB Small Business Optimism Index showed the fifth consecutive monthly decline in expected business conditions, reaching the lowest level since 2024. At the same time, labor cost was cited as the single most important problem facing business owners by 14% of respondents, the highest reading in survey history. Small businesses’ plans to create new jobs within 3 months were a net 9%, the lowest since May 2020. Initial Jobless Claims for the week ended June 6 were 229,000, rising to the higher end of the range seen in the first half of 2026. The Preliminary June Consumer Sentiment report showed a strong rebound in sentiment as gasoline prices cooled from May highs. Consumers broadly showed improvements in present conditions and future expectations across personal finances and business expectations.

SpaceX became the biggest IPO in history on Friday, raising $75 billion and minting Elon Musk the world’s first trillionaire. SPCX stock closed up 19.22% from its opening price, valuing the company at $2.11 trillion and placing it as the 8th largest public company by market capitalization. Oracle reported Q4 2026 earnings results this week, growing revenues 21% YoY and cloud revenue by 47% YoY. While revenue and EPS beat consensus estimates, CapEx of $16.5 billion was significantly higher than expectations, and ORCL shares were pressured due to the increasing AI spending. Adobe also reported Q2 2026 earnings this week, surpassing consensus estimates on revenue and EPS, but the announcement that CFO Dan Durn would be departing the company following CEO Shantanu Narayen’s resignation earlier this year pressured ADBE shares. Next week, investors will look to Federal Reserve Chairman Kevin Warsh’s first FOMC meeting and rate decision on Wednesday, at a time when recent data has shown inflationary pressures have been outpacing labor market concerns.

Friday’s Close (Weekly Performance)

S&P 500 7,431.46 (+0.65%)

Nasdaq 25,888.84 (+0.70%)

Dow Jones 51,202.26 (+0.66%)

Thank you Blue Room Senior Analyst JARED FENLEY.

Maury Raycroft

Jefferies

Hi everyone, my name is Maury Raycroft and I'm one of the biotech analysts at Jefferies. I'd like to welcome the Precision Biosciences team. Maybe if you guys want to give an intro and a brief intro to the company as well. A lot going on with the company, so I'll let you take over. Thanks for joining us today.

Adam Mischler

Senior Scientist, Translational & Research Lead of Duchenne Muscular Dystrophy Program

So I'm Adam Mishler, translational and research lead of our Duchenne muscular dystrophy program.

Emily Harrison

Lead of Chronic Hepatitis B Translational Program

Emily Harrison, lead of the HBV translational program.

Michael Amoroso

President & Chief Executive Officer

Maury, thanks for having us. Michael Amoroso, President and CEO of Precision. Precision is a gene editing company in vivo gene editing only. We are applying our proprietary ARCUS technology, which has some very unique properties to it. We talk about the cut, very unique cut type, the size and the simplicity. Those have some advantages with the types of programs, how you can deliver the gene editor, the type of repair mechanism for different functions like excising or adding function insertion. So we apply that in our clinical programs where it makes the most sense.

Precision is out of Durham, North Carolina. Been public since 2019, have about 100 employees. And right now we are focusing on HBV, chronic hepatitis B. We just showed at the EASL converse some really groundbreaking data of what PBGENE-HBV, our ARCUS gene editor wrapped in an LNP can do in chronic hepatitis B directly eliminating cccDNA. We'll start in the clinic in the second half here in Duchenne muscular dystrophy very soon. We've got an IND approved. We have our onboarding sites. And next step is clinical initiation.

Maury Raycroft

Jefferies

Got it. Yeah, it's a great intro. And you mentioned the update at EASL recently. There you had the first demonstration that cccDNA can be eliminated from the liver of a patient with chronic HBV. What's been the feedback from KOLs and investors since that update?

Michael Amoroso

President & Chief Executive Officer

Yeah, so Emily was on the ground in Barcelona and maybe I'll let you start of some of the buzz and excitement we heard in Barcelona and I'll kind of cap us.

Emily Harrison

Lead of Chronic Hepatitis B Translational Program

Yeah, I think this is something the field has been waiting for for decades to try to find a technology that can directly target and eliminate the cccDNA. So there was a huge positive reception at the data showing that we can actually cut and eliminate cccDNA to drive, importantly, the loss of a key biomarker for cccDNA — pgRNA. So there was a very positive reception.

Michael Amoroso

President & Chief Executive Officer

Yeah, and I would say more obviously, we spent a lot of time together in the last week or so. I'd say the understanding that you could dream about a complete viral cure, right? I'll remind everybody, cccDNA is the only source in this chronic hepatitis B that makes infectious virions that can make replicating virus. It's during that stage of replication where some virus gets integrated in the host genome fragments, but those can never replicate. Those are not replication active. That's when cancer happens in patients. So you really need to cure the source.

To date, in drug development in HBV, we have tried anything we could do with the tools we had, targeting downstream viral transcripts and markers to try to turn the immune system on to attack the cccDNA, but we've never been successful as an industry. This is the first time we have proof of direct targeting and elimination, biopsy proof, blood marker proof with pgRNA of elimination of the replicating viral source.

This month, consumer sentiment ticked up about four index points, or 9%, to 48.9, with consumers experiencing some relief due to the early-month easing in gasoline prices.

This measured improvement in sentiment was widespread, seen across age, education, and political party. Lower-income consumers exhibited a particularly strong sentiment increase, consistent with the fact that gasoline comprises a larger share of their budgets.

Overall, assessments and expectations of personal finances and business conditions all rose this month.

Even with June’s early gains, however, views of the economy are still relatively dour. Sentiment is currently 13% below January 2026 and 19% below a year ago, as consumers remain focused on kitchen table issues. They feel burdened by the recent escalation in inflation and worry that higher inflation could remain stubborn going forward, particularly in the short run.

Interviews for this release were completed between May 19 and June 8.

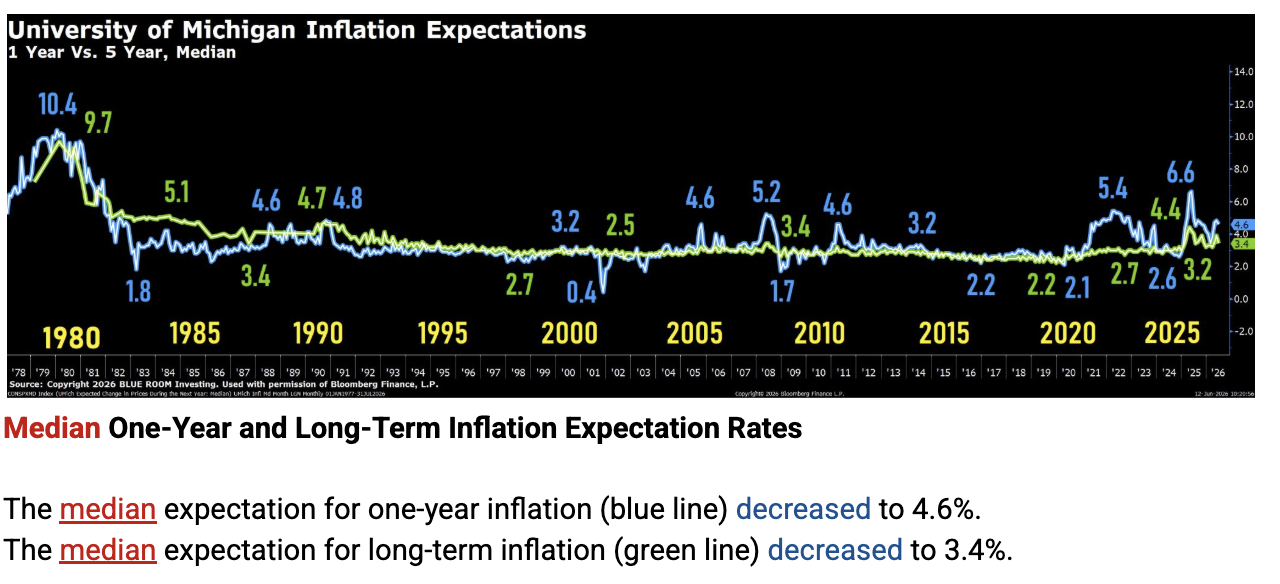

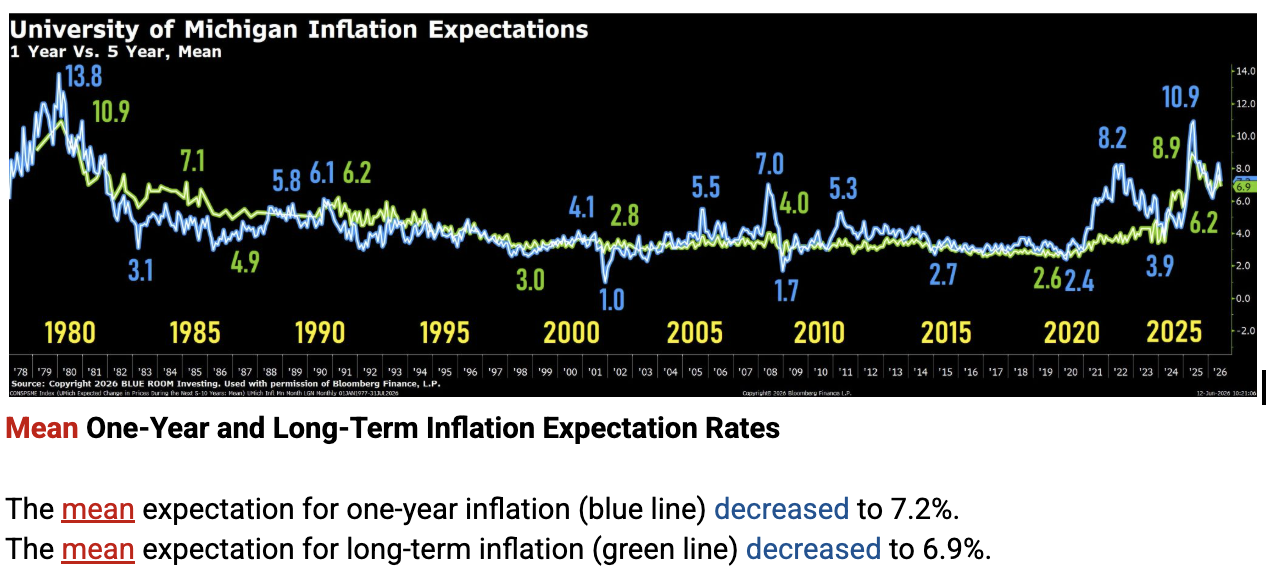

Year-ahead inflation expectations inched down from 4.8% in May to a still-elevated 4.6% this month. The current reading substantially exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict, along with all 2024 readings.

Long-run inflation expectations fell back from 3.9% last month to 3.4% in June, remaining notably higher than the 2.8% to 3.2% range seen in 2024.

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.