Weekend Update #183

Thank you for your continued support and engagement. Each week, we're sharing what companies we're researching and the what, the who and the how that we think makes the companies interesting and unique. This roundup is brought to you weekly by a group of interns, creative minds, artists and investors who believe that through best in class investing along with the democratization of financial education we can do great things together. Enjoy, Explore and Share.

The S&P 500 closed at a new all-time high on Thursday and settled just below that mark to end the week, driven by increased hopes for a soft landing following positive CPI and PPI inflation data. The index is powered by increasingly concentrated gains from the likes of the Magnificent Seven and companies benefitting from AI excitement, despite lingering concerns about consumer strength and geopolitical risks. French President Emmanuel Macron called a surprise parliamentary election following his party’s loss of voters at the European Parliament elections, opening the door for Marine Le Pen’s National Rally party to gain parliamentary control. The resulting political uncertainty has rattled European markets with French stocks losing $210 billion in value this week — consequences that risk impacting even U.S. markets. Domestic concerns were voiced by Pimco’s John Murray this week as he flagged additional regional bank failures yet to come due to their high exposure to commercial real estate loans.

In economic news for the week, core CPI rose 0.2% month-over-month in May with the year-over-year reading at 3.4% — the lowest reading since April 2021. The report was an encouraging sign that inflation is back on a downtrend after initial 2024 readings sparking concern over sticky inflation. PPI followed CPI showing more progress on inflation with its largest decline since October 2023. Core PPI was 0.0% month-over-month and 2.3% year-over-year in May. The toll that high interest rates and the Fed’s fight against inflation are having on the economy was evident in Friday’s consumer sentiment report for May — The index fell to a 7-month low on rapidly deteriorating consumer views on their financial situations with slight increases to inflation expectations.

As the Federal Reserve has worked to lay the groundwork for, equities remained data-focused and surged on a positive CPI report on Wednesday while the more hawkish-leaning tone of the FOMC’s SEP and Fed Chair Powell’s commentary was digested as more or less “old news”. The median member of the FOMC now expects just one rate cut in 2024 with 4 rate cuts to come in 2025 — down from the prior March expectation for 3 rate cuts this year. FOMC members’ real GDP expectations ticked up, but higher inflation expectations and more uncertainty around those projections caused the committee to pencil in a more hawkish view on interest rates. The FOMC’s dot plot showed a bit more consensus building around the projected interest rate path which can be taken as a positive for markets. If inflation data continues to come in cool, the market is betting the FOMC could easily implement two rate cuts this year.

Friday’s Close

(Weekly Performance)

S&P 500 5,222.68 +1.58%

Nasdaq 16,340.87 +3.24%

Dow Jones 39,512.84 -0.54%

Thank you Blue Room Analyst JARED FENLEY.

This week, Federal Reserve Board Chairman Jerome Powell’s speech lifted stocks as the Fed’s key interest rate was maintained and he indicated only one potential rate cut this year. This came despite political turmoil in Europe weighing heavily on share prices in the region. Elections in France and contagion to other countries like Italy and Spain are triggering debate about future stability in the Eurozone. For now, we believe that the spillover into the US will be limited but if France and others move in the same direction as Great Britain i.e. BREXIT, we will have to watch our exposure to the region even closer.

For the second week in a row, our best performing long positions were Nvidia and Hewlett Packard Enterprises (HPE). AI continued to take center stage and we expect this to continue for the foreseeable future. Nvidia is helping to lead this latest technological revolution and HPE is prospering as well. Our option position in Shopify also added to weekly performance after a Wall Street analyst upgraded their recommendation. The basis for the upgrade was valuation and Shopify’s competitive position.

We had a more challenging week in our short potions. Arm Holdings, Adobe and Arista Networks were all up sharply, Arm jumped on news of its inclusion in the NASDAQ 100 Index. Adobe posted their biggest gain in more than four years as its latest announcement suggests that customers are adopting its new AI based tools. Arista was another mover on AI related bullish commentary and sell-side validation. It seems as if any mention of AI in a company release has a positive effect on its share price. We know that not all companies will experience the same magnitude of success in this space so we will continue to bet against those that we feel are overvalued relative to our forecast of their potential growth rates. For now, we are holding steady all three short positions.

Thank you Blue Room Investing President JOHN FENLEY

Mike Cyprys — Morgan Stanley

Good afternoon, everyone, and thanks for joining us here at the Morgan Stanley Financials Conference. I'm Mike Cyprys, Equity Analyst covering brokers, asset managers and exchanges for Morgan Stanley Research. And for our next session, it's my pleasure to welcome Greg Tusar, Vice President of Institutional Products at Coinbase.

With over $330 billion of assets on the platform as of the first quarter, Coinbase is a crypto platform that facilitates trading, staking and custody of crypto tokens as well as provides broader services to the crypto ecosystem. Greg, thanks so much for joining us.

Greg Tusar — VP of Institutional Products

Thanks for having me. Appreciate it.

Mike Cyprys — Morgan Stanley

Great. So I've been asked to read the Safe Harbor statement before we start. I'd like to remind you that during today's chat, Greg may make forward-looking statements. The actual results may vary materially from today's statements due to risks, uncertainties and other factors that are described in SEC filings. Our discussion today may include references to non-GAAP financial measures and a reconciliation of non-GAAP financial measures is available in the company's latest Shareholder Letter. That's a mouthful.

All right. With that out-of-the way, why don't we dig in here? You have a really interesting background, Greg, in market structure spanning a number of decades, including your time at Goldman Sachs. I believe you had -- you were leading a company that sold itself, that then sold itself to Goldman. You were at KCG for some time as well. You founded a crypto prime broker Tagomi, which you sold to Coinbase in 2020. You now run the Institutional Products business at Coinbase.

So what attracted you to the crypto industry after spending so many years in more traditional finance, more on the equity side? And maybe talk about your role and responsibilities today and how you're spending your time?

Greg Tusar — VP of Institutional Products

Sure, happy to. That was a good summary. So this is 32 years for me, somewhere at the intersection of technology and finance. I started, as you said, at the beginning of what by sure luck turned out to be the start of electronic trading and equities, and spent the bulk of it at Goldman Sachs. And then entered the world of crypto and digital assets in 2017, something about it seemed inevitable to me then and it does now.

And the idea was to bring the learnings from helping institutions learn to trade electronically in equities and foreign exchange and fixed income into the world of crypto and digital assets. So we co-founded the company in 2017 called Tagomi, and we were then acquired by Coinbase in 2020. And the idea in 2020 was to marry what we built, which was advanced trading together with what Coinbase had at the time, which was really centered around custody first and foremost. And marrying those two things together like chocolate and peanut butter and we -- that became what we call Coinbase Prime. And so, we've been on this great journey since then building an institutional business. And there are some learnings from prior market structures like we were talking about before, but it is in many ways sort of its own asset class with its own idiosyncrasy.

Mike Cyprys — Morgan Stanley

Great. And when most people think about Coinbase, they often think about the direct-to-consumer business, but there's also a fast-growing and important institutional business under their hood as well. So maybe you could help contextualize this institutional business, how meaningful is this?

Greg Tusar — VP of Institutional Products

Yeah. Well, of the assets that you said, about half of that are actually held by institutions. So as of the end of the first quarter, it was about $170 billion of assets. And the word institutional in crypto is a funny thing. It means a lot of different things to a lot of different people. And so for us, it covers a lot of surface area. There are market makers and professional traders, and that's generally in crypto what people mean by institution. But we also cover ETF issuers, asset managers, pensions, endowments, corporate clients. So institutional at Coinbase means a lot of different things.

And again, it started right around 2018 with the birth of the custody business and we've been building concentrically around that custody is for us, the first and most important thing that our institutional customers come to us for the safekeeping of private key material might be the single most important thing we do as a company. But we've been building other services around that over time.

So Zooming out for a minute, the way we think about the institutional business, there's three main pillars. There’s what we call Coinbase Prime. So that's custody, that's trading, that's financing, staking. We now have a Web3 wallet product, and from there, you can do things onchain like governance and other things. And the idea is to have a product portfolio and a platform that makes it easy for customers to go from one thing to the next. And that's our Prime product. And that began again with the acquisition of Tagomi in 2020, and before that, the acquisition of Xapo. So this has been both an organic story and an inorganic story over time.

The second pillar, we call markets and that's what has our underlying spot market that has our US CFTC-regulated futures market and has our new international market for non-US customers.

And then the third pillar, which is the most nascent and came through the acquisition of a company called One River Digital Asset Management is our asset management business. Coinbase Asset Management is an attempt to have something on the shelf that will appeal to asset owners and others that want all of these services, but in a fiduciary wrapper. And so the idea is to have each of these offerings for different client types.

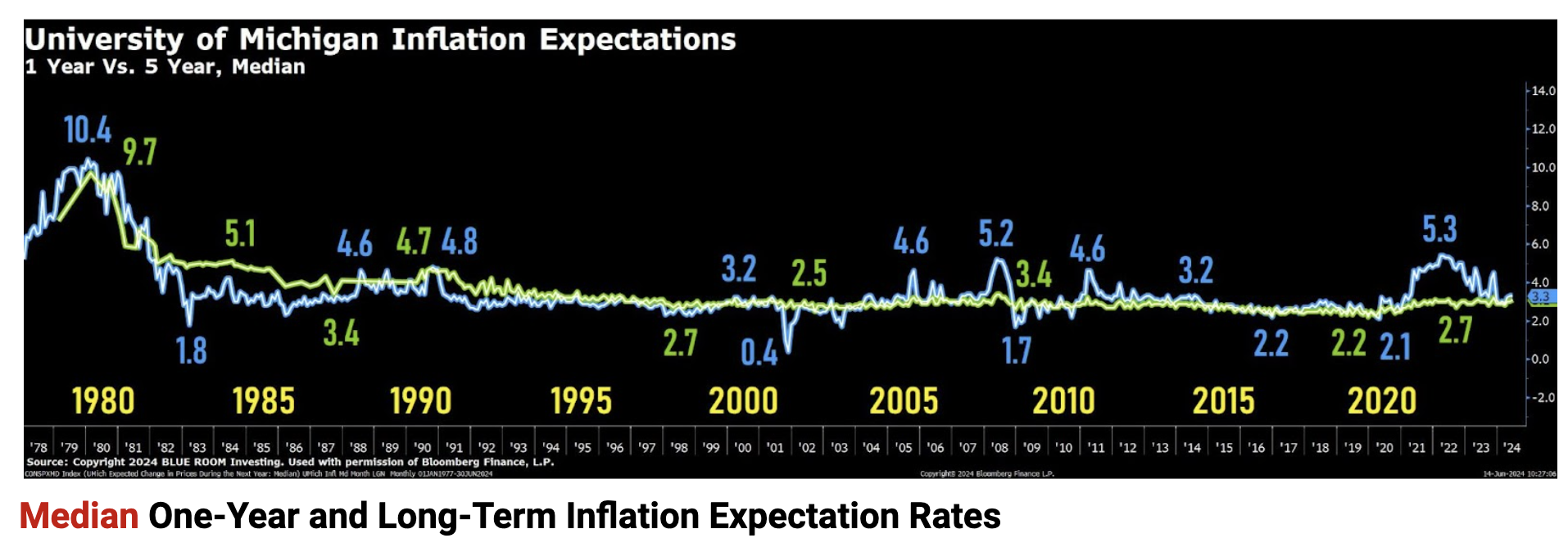

Median One-Year and Long-Term Inflation Expectation Rates

The median expectation for one-year inflation (blue line) remained unchanged at 3.3%.

The median expectation for long-term inflation (green line) increased to 3.2%.

At 65.6, consumer sentiment was little changed in June. This month’s reading was a statistically insignificant 3.5 index points below May and within the margin of error.

Sentiment is currently about 31% above the trough seen in June 2022 amid the escalation in inflation.

Assessments of personal finances dipped, due to modestly rising concerns over high prices as well as weakening incomes. Overall, consumers perceive few changes in the economy from May.

Mean One-Year and Long-Term Inflation Expectation Rates

The mean expectation for one-year inflation (blue line) remained unchanged at 5.5%.

The mean expectation for long-term inflation (green line) increased to 5.3%.

Year-ahead inflation expectations were unchanged this month at 3.3%, above the 2.3-3.0% range seen in the two years prior to the pandemic. Long-run inflation expectations inched up from 3.0% last month to 3.1% this month — The June reading should be interpreted as essentially unchanged from May. Long-run inflation expectations have been remarkably stable over the last three years but remain elevated relative to the 2.2-2.6% range seen in the two years pre-pandemic.

All of these patterns are visible when looking at trends within phone interviews alone or web interviews alone, and thus they are not artifacts of the survey’s methodological transition.

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been modest further progress toward the Committee’s 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals have moved toward better balance over the past year. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage backed securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas l. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowan; Lisa D. Cook; Mary C. Daly; Phillip N. Jefferson; Adriana D. Kugler, Loretta J. Mester; and Christopher J. Waller.

Salveen Richter — Goldman Sachs

Great, good morning, everyone. Thank you so much for joining us. Really pleased to have the Vertex team here with us. Today, we do have David Altshuler, Chief Scientific Officer as well as Charlie Wagner, CFO.

Maybe to start here, could you give us a snapshot of the business today and what we should anticipate in terms of strategy and commercial execution and pipeline in the second half of the year?

Charles Wagner — Executive VP and Chief Financial Officer

Yeah. Listen, Salveen, thank you for hosting. We're happy to be here and good morning, everybody. I would just say this is an incredibly exciting time at Vertex and the Company has never been in a stronger position. If you listen to our recent Q1 earnings call, we continue to grow in CF, TRIKAFTA continues to grow. We're expanding geographically. We are increasing our penetration into younger age groups and the business just continues to execute very consistently and well.

Not only are we growing in CF, we continue to innovate. There's a lot of interest, of course, in our collaboration with Moderna for our mRNA program for CF, and we'll have more to say on that program late this year, early next year. I would say significantly, 2024 also represents an important milestone in terms of commercial diversification for the Company with the launch of CASGEVY, our therapy for sickle cell disease and beta thalassemia.

The early launch is going incredibly well. And keep in mind that we received a number of approvals in different geographies around the world in a very short period of time. We've commented that a number of patients have already had cell collection and have begun the patient journey and the interest from the patient and physician community is outstanding.

And so we're really excited about that launch as well. We recently closed on the acquisition of Alpine Immune Sciences, which brings with it an asset called Povetacicept or POVE. It's Phase 3 ready in IgA nephropathy and it's in basket trials, Phase 1/2 basket trials in a number of renal indications and cytopenias represents -- truly represents a pipeline and a product and something that we're very excited about.

And so overall, the business continues to grow. The pipeline has never been broader. We will have updates on some of our other pipeline programs this year, notably type 1 diabetes, mRNA, as I described and others late this year, early next year. And so in terms of both growth and diversification and the pipeline, the Company is really in a fantastic place. And maybe that's a great place to start for this conversation.

Salveen Richter — Goldman Sachs

Perfect. Let's maybe start with the commercial aspect here. So on your pain programs, you do have an NDA submission for your drug for acute pain. Help us understand the go-to-market strategy here and how you're negotiating in terms of contracting, thinking about pricing?

Charles Wagner — Executive VP and Chief Financial Officer

Yes. So with acute pain, we have a rolling submission and we'll have more updates on that soon, it represents an incredible opportunity. As we look at the treatment of pain with VX-548, we see the ability to transform the treatment of pain. There is a lot of unmet need, there's a lot of undertreated pain because quite candidly, the standard of care right now, particularly with opioids in acute is not very attractive for many patients.

And so we see a huge opportunity here. Commercially, we think it's a multi-billion dollar opportunity and one that we're poised to go after. As we think about the commercial opportunity though, we want to take a very focused approach that's consistent with the Vertex specialty commercial model. And so for example, if you look at acute pain, there are over 80 million people a year who are treated for acute pain in the US, represents north of 1 billion treatment days in a given year.

Roughly 50% of the volume is either prescribed in an institution or at the time of discharge. An institution might be a hospital, might be a surgical center, but the institutional setting is really significant in terms of prescribing. And within that, we see a high concentration. There are roughly 2,000 hospitals that roll up into 200 IDNs that drive the majority of prescribing around acute pain.

And so we see a real opportunity to focus there, particularly working with key opinion leaders in institutions like that, whether they be orthopedic surgeons, plastic surgeons, ER docs, pain specialists, anesthesiologists, all of those really carry a significant share of voice in those institutions.

So, we're going to target our commercial efforts early. We think we can do that with a specialty sales force that's targeted at the physician and hospital level with key account managers that are targeted at the IDN level and then with MSLs or Medical Science Liaisons, really helping to drive a high science approach to this.

We also are looking at opportunities for inside sales and digital enablement to make sure that we're amplifying the voice of the sales force. And so all of that is in great shape. We are essentially going to be fully staffed in pain for the commercial organization in the current quarter. And so we feel very, very good about that.

In terms of next steps, in the institution, right now, we're focused on compliant information exchanges in this pre-approval setting, but we know that we're going to work through P&T committees. We know that we need to get on formulary, we know we're going to be talking to PVMs, we know we're going to be talking to payers. Those conversations are already happening at this point.

And there is just a ton of interest in an alternative to opioids. So those conversations are going very well. There's a lot of work to do to make all of those things happen, obviously, but we've built a great team and feel really confident about our ability to launch upon approval.

Salveen Richter – Goldman Sachs – Analyst

Great. Good afternoon, everyone. Thank you so much for joining us. Really pleased to have Stephen Hoge, President of Moderna with us this morning.

Stephen Hoge – President

Thanks for having us.

Salveen Richter – Goldman Sachs – Analyst

After having just announced some news today on the COVID-flu combo, perhaps before we get into that, some big-picture questions, Moderna has over 40 programs in development. And in the context of R&D spend management, what is your strategy for pipeline prioritization?

Stephen Hoge – President

Great question. So, well, thank you, first of all. It's really exciting to be here, my first time in Miami with you too. So, first on the question of prioritization, as you know well, because you've followed us for years, we are a platform company. And so we actually start with the question of what can our platform technology, which in our case is messenger RNA – what can it do? And we don't sort of say what we'd like it to do, we say, what is the pharmacology that it can do now. And as we've articulated, including our last R&D Day, there are really four pillars where we think our technology is mature and we're scaling, we call them modalities.

The first is respiratory vaccines. The second is vaccines against other viruses, so latent viruses, and other infections. The third is our work in oncology, principally around our INT program with Merck. And then the fourth is rare diseases, so expressing proteins in the liver. And in those four modalities, we're advancing anywhere between five and 10 medicines. Because we're a platform company, we really think it's important that it's multiple medicines in those modalities because the probability of the success of the first one might be not that different from other technologies, but the second, third, fourth, and fifth can be quite high.

And so what we try to do is advance a broad portfolio across those four modalities and over time add more. Now when it gets down to the question of how do we pick within those modalities, a lot of that boils down to unmet need and where we see the opportunity – generally where there are things that we think our technology can uniquely do, like in rare diseases or cancer or in respiratory combinations. We will prioritize those and advance them forward. And that's one of the most difficult parts of my job often as the Head of R&D is working with the team to say we can't quite prioritize that program now and we hope to get it in the future.

— Press Release —

June 10, 2024

The Federal Reserve Bank of New York’s Center for Microeconomic Data today released the May 2024 Survey of Consumer Expectations, which shows inflation expectations declined at the short-term horizon, remained unchanged at the medium-term horizon, and increased at the longer-term horizon.

Labor market expectations were mixed. Households’ expectations for the stock market improved, reaching a three-year high. Households were also more optimistic about their financial situation a year from now.

INFLATION

Median inflation expectations at the one-year horizon declined to 3.2% in May from 3.3% in April, were unchanged at the three-year horizon at 2.8%, and increased at the five-year horizon to 3.0% from 2.8%. The survey’s measure of disagreement across respondents (the difference between the 75th and 25th percentile of inflation expectations) decreased at the one-year horizon, increased at the three-year horizon, and remained unchanged at the five-year horizon.

Median inflation uncertainty — or the uncertainty expressed regarding future inflation outcomes — increased at the one- and three-year horizons and declined at the five-year horizon.

Median home price growth expectations were unchanged at 3.3%.

Andrea Tan — Goldman Sachs

Michael, as you think about the last 12 months, Precision has gone through a strategic transition — one that has now put you squarely on path to be an in vivo gene editing company. Maybe speak to us about what drove that decision? What does that mean for Precision as a company?

Michael Amoroso — President & Chief Executive Officer

First and foremost, Precision has always been a gene editing company

The platform that Jeff created with ARCUS is their own IP, maybe not as well known as some of the others

Not everyone can touch and handle it

Their first programs for ARCUS were ex vivo applications for CAR T

Those were important programs for patients

They’ve had some really nice data there, before they divested those programs to partners

The landscape changed, the cost of capital changed

The core capability of Precision is ARCUS

It’s a highly differentiated gene editing platform

All of the gene editing platforms are CRISPR

Base and prime are derivatives of that

Those are good technologies

Most of them are really good at delivering gene knockouts

ARCUS can do those knockouts, but it was designed to do sophisticated edits — such as adding DNA, or excision of large base pairs

Early programs are eliminations

With HBV, they’re getting rid of the entire viral genome

This technology is highly differentiated, and what that means is they can apply that in much larger areas for millions of patients with afflicted diseases

When the landscape changed, when they got to the inflection point, they thought they’d take the CAR T programs across the line to the first BLA and then partner it

When they got the pivotal feedback from the FDA, they thought it was the right time to partner it off — with Imugene for cancer rights to azer-cel and TG Therapeutics for autoimmune, who’s already in the multiple sclerosis space

Operationally, they wanted to focus fully on the in vivo capability

That’s really what Precision was built on

That’s where they are now — one platform, HBV as the lead program, primary mitochondrial myopathy as the second

The landscape helped them get to the pivot faster, but it was always the plan for Precision

They’ve gotten a lot of feedback that now investors know exactly that Precision represents a gene editing company

Andrea Tan — Goldman Sachs

Jeff, as Michael alluded to, the ARCUS platform — help us understand how that’s differentiated from other gene editing technologies?

Jeff Smith — Chief Research Officer

There are three key advantages to ARCUS over all the other gene editing platforms:

1. The very unique cut that ARCUS generates

ARCUS is derived from a completely different scaffold protein than all of the other gene editors

They’ve maintained the evolved function of that base protein to be available to insert DNA using homology-directed repair

A lot of that tracks back to the unique cut that the enzyme generates — a staggered cut

That allows it to insert with really high efficiency, even in non-dividing cells, which allows them to tackle different patient populations than a lot of competitors

2. Size

ARCUS is the smallest gene editor on the market

It is substantially smaller than nano CRISPRs that come out

That gives a few advantages: it allows them to deliver both by LNP and AAV, to be able to do sophisticated edits beyond the liver in other tissues

It also gives safety — they’re able to package a more potent, cleaner drug product in LNP like with HBV

It allows them to gain access to target sites, such as in viral DNA for the HBV program

3. Simplicity

ARCUS is the only single-component gene editor

If you had to deliver something to get a job done, all in one truck, that’s a lot easier than having to deliver 5 different vehicles and get them there at the same time

ARCUS is able to be delivered in a compact way, in a single delivery vehicle

That helps lower the dose

The DNA binding that finds the correct binding site is fully integrated into the cutting — only when you find the correct site does it actually do the cutting

WELCOME SUMMER 2024 INTERNS

June 13, 2024 BLUE ROOM Meeting 152

Thursday

June 13, 2024

12 PM

The 2024 Summer Internship started this week, which means Intern Introductions!

__________

Read our weekly newsletter!

+++ CONGRATULATIONS +++

ERIKA & KELLY WHITAKER

+ ID EST HOSPITALITY

Monday, June 10, 2024

Lyric Opera House

Chicago, Illinois

OUTSTANDING RESTAURATEUR

Erika and Kelly Whitaker

Id Est

Boulder, Colorado

The Wolf’s Tailor

Denver, Colorado

BRUTØ

Denver, Colorado

BASTA

Boulder, Colorado

Hey Kiddo — Ok Yeah!

Denver, Colorado

Nonesuch

Oklahoma City, Oklahoma

Dry Storage

Boulder, Colorado

ID EST

Boulder, Colorado

10% OF ALL BLUE ROOM REVENUES GO DIRECTLY TO FUND OUR NON PROFIT TOGETHERISM.

WE CAN ACCOMPLISH ANYTHING TOGETHER.

These materials do not purport to be all-inclusive or to contain all the information that a prospective investor may desire in considering an investment. These materials are intended merely for preliminary discussion only and may not be relied upon for making any investment decision. Any discussion or information contained in this presentation does not serve as a receipt of, or as a substitute for, personalized investment advice from Blueroom or your advisor.

This publication does not constitute an offer to sell or a solicitation to buy any securities in any fund, market sector, strategy or any other product. Investing is speculative and involves substantial risks (including, the risk of loss of the investor’s entire investment). Past performance is not indicative of future results, and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable.

For more information about us and our general disclosures contact us directly.